Table of Contents >> Show >> Hide

- The Big Picture: Mortgage Rates Are High Because Money Is Still Expensive

- Why Mortgage Rates Stay Elevated

- Why High Rates Hurt So Much More Right Now

- What This Means for Buyers and Sellers

- Could Mortgage Rates Fall Soon?

- How Buyers Can Respond Without Losing Their Minds

- Experience Section: What High Mortgage Rates Feel Like in Real Life

- Conclusion

- SEO Tags

For a lot of Americans, mortgage rates still feel like the unwelcome houseguest who said they were “just stopping by for a minute” and then settled into the recliner for three years. Even after cooling from the eye-watering peaks of late 2023, mortgage rates remain high enough to make buyers blink twice, refresh rate pages compulsively, and suddenly become very interested in the emotional stability of the 10-year Treasury yield.

So, why are mortgage rates still so high? The short answer is that mortgages do not live in their own cozy little universe. They are shaped by inflation, bond markets, Federal Reserve policy, investor nerves, housing supply, and the extra premium lenders and investors demand when the economy feels unpredictable. In plain English: borrowing money to buy a home is more expensive because the wider financial system still says risk is not cheap.

This article breaks down what is really happening, why mortgage rates are staying elevated, and what it means for buyers, sellers, and anyone currently whispering “maybe next spring” into a Zillow tab.

The Big Picture: Mortgage Rates Are High Because Money Is Still Expensive

Mortgage rates are high because the broader cost of money is still elevated. Lenders do not simply wake up in the morning, spin a wheel, and land on 6.11% because the universe enjoys chaos. They price loans based on what investors demand to hold mortgage-backed securities, where Treasury yields are trading, how sticky inflation looks, and how likely it is that the Federal Reserve will keep rates higher for longer.

Even when the Fed is not directly setting mortgage rates, its policy choices influence the entire interest-rate landscape. If investors believe inflation may linger, they usually demand higher returns on long-term bonds. Since mortgage pricing tends to move with long-term bond yields, especially the 10-year Treasury, home loan rates stay elevated too.

That is why mortgage rates can remain frustratingly high even when people hear chatter about future Fed cuts. The mortgage market is forward-looking. It cares less about wishful thinking and more about whether inflation is truly under control, whether bond buyers feel confident, and whether investors think the economy is headed for stability or another plot twist.

Why Mortgage Rates Stay Elevated

1. Inflation Has Cooled, but It Has Not Fully Relaxed on the Couch

Inflation is still one of the biggest reasons mortgage rates remain high. When inflation runs above the comfort zone, investors worry that fixed-income returns will lose purchasing power over time. To compensate, they want higher yields. That pushes up Treasury yields and, by extension, mortgage rates.

Even modest inflation anxiety matters. Mortgage rates do not need runaway inflation to rise. They just need enough concern to make bond investors cautious. In 2026, that caution is still very much alive. And when new pressures appear, such as higher energy costs or geopolitical disruptions, markets quickly start repricing risk.

In other words, inflation does not have to be screaming to keep mortgage rates high. A persistent, annoying mutter is often enough.

2. The 10-Year Treasury Yield Is Still Doing Heavy Lifting

The 30-year fixed mortgage does not move in lockstep with the federal funds rate. Instead, it tracks more closely with the 10-year Treasury yield. That is the market number many buyers should watch if they want a better sense of where mortgage rates may head next.

When the 10-year yield rises, mortgage rates usually follow. Why? Because mortgage-backed securities compete with Treasurys for investor attention. If Treasurys are paying more, mortgage investors want more too. Simple, ruthless, very Wall Street.

That is a major reason rates feel sticky. Even when short-term policy rates stop climbing, long-term yields can stay elevated if markets expect inflation to remain stubborn, government borrowing to stay heavy, or economic uncertainty to linger. Mortgage rates are basically saying, “I know the Fed might ease eventually, but I have trust issues.”

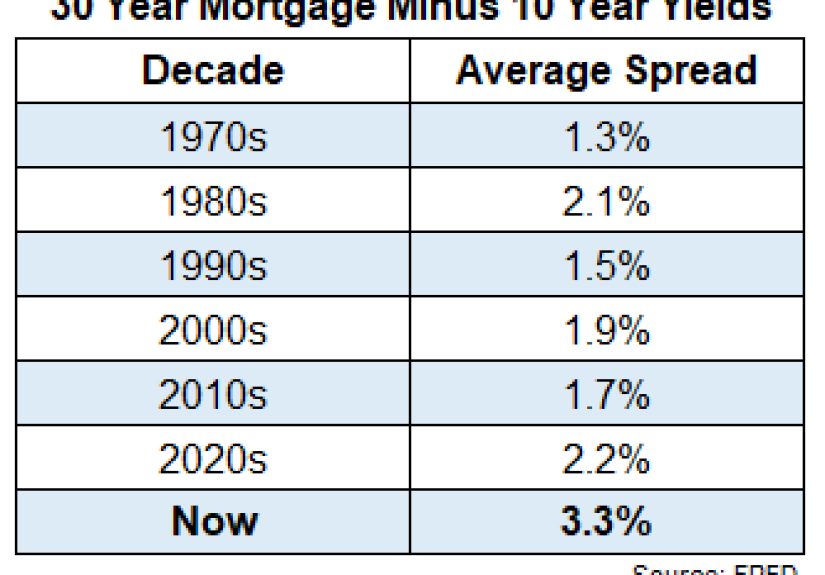

3. The Mortgage-Treasury Spread Is Still Wider Than Normal

One of the more underappreciated reasons mortgage rates feel painfully high is the spread between mortgage rates and the 10-year Treasury yield. That spread widened in recent years and has stayed larger than many borrowers would prefer.

This spread reflects extra compensation for risk. Mortgage-backed securities carry complications that plain Treasurys do not. Borrowers refinance. Loans get prepaid. Market volatility changes investor demand. And when there is uncertainty about inflation, housing turnover, or future policy, investors demand a bigger cushion.

So even if the 10-year Treasury is not at some shocking historical extreme, mortgage rates can still look nasty because the premium layered on top remains fat. It is not just the benchmark yield. It is the stress surcharge.

4. The Fed Matters Indirectly, and Markets Listen Closely

The Federal Reserve does not set 30-year fixed mortgage rates directly, but it absolutely shapes the environment around them. When the Fed keeps short-term rates elevated to control inflation, financial conditions stay tighter across the economy. Banks, lenders, and investors all adapt to that reality.

Markets also react to what they think the Fed will do next. If traders believe rate cuts will be delayed, mortgage rates can stay high even before the Fed does anything new. If investors think inflation could flare back up, the bond market may push yields higher on its own.

That is why “the Fed might cut later” does not automatically equal “your lender just offered you 4.5%.” Mortgage rates respond to expectations, not just decisions.

5. Geopolitical Shocks Keep Bond Markets Jumpy

Mortgage rates are not driven only by domestic housing math. Global events can push them around too. When geopolitical tensions rise, energy prices can increase, inflation worries can return, and bond markets can move sharply. That can feed directly into mortgage pricing.

This is one reason mortgage rates can jump even when housing data itself seems calm. A buyer may be carefully comparing neighborhoods and school districts while the bond market is busy having an existential crisis over oil, inflation, and global conflict. The borrower just sees a worse quote the next morning.

Mortgage rates are not dramatic for the fun of it. They are dramatic because markets are dramatic.

Why High Rates Hurt So Much More Right Now

Home Prices Are Still High

High mortgage rates would be difficult enough on their own. The real problem is that they are arriving on top of elevated home prices. Even where price growth has slowed, values remain far above pre-pandemic levels in many markets. That means buyers are getting hit from both directions: a bigger loan amount and a more expensive rate on that loan.

A one-point move in mortgage rates might sound manageable in theory. In practice, it can add hundreds of dollars to a monthly payment when the home itself already costs close to $400,000 or more. The math gets ugly fast.

Inventory Is Still Too Tight

The housing market is still dealing with a supply problem. Inventory has improved in some places, but it remains below pre-pandemic norms nationally. And affordable starter homes are especially scarce.

That matters because low supply props up prices and limits buyer negotiating power. If more homes were available, high rates might be partially offset by softer prices. But when buyers compete for too few listings, affordability stays squeezed.

The Rate-Lock Effect Is Still Real

Millions of homeowners locked in mortgage rates below 4%, and many are not eager to trade those loans for a new one above 6%. That “rate-lock” effect discourages existing owners from selling, which keeps resale inventory tight.

This creates a weird market dynamic. Many current owners would like more space, less space, a different school district, or a shorter commute. But moving means giving up a mortgage rate that now looks like a museum exhibit from a lost civilization. So they stay put, and fewer homes hit the market.

Fewer listings mean less relief for buyers. Less relief for buyers means affordability stays lousy. And affordability staying lousy makes every mortgage rate look even worse.

What This Means for Buyers and Sellers

For Buyers

Buyers are dealing with a market where waiting for a magical rate collapse may not be the best plan. Could rates fall further? Sure. Could they also bounce around and remain elevated? Absolutely. The lesson is not “panic buy.” It is “buy when the payment works for your life, not when the headlines flatter your hopes.”

That means focusing on affordability first. Monthly payment, cash reserves, closing costs, and long-term comfort matter more than winning a guessing game against the bond market. If a home fits your needs and budget now, refinancing later may be possible if rates drop. But if the payment is already stretching you like old elastic, a lower future rate is not a solid financial strategy. It is fan fiction.

For Sellers

Sellers face their own version of the same mess. Many do not want to list because they would become buyers in the same rate environment. That keeps inventory constrained, but it also means fewer shoppers can afford premium pricing.

In some markets, well-priced homes still move quickly. In others, buyers are more selective and no longer willing to throw money at every property with a front door and a functioning mailbox. Sellers who price based on 2021 vibes may be in for a humbling experience.

Could Mortgage Rates Fall Soon?

They could, but probably not in a clean, dramatic, movie-trailer kind of way. Mortgage rates are more likely to drift than collapse unless inflation cools decisively, Treasury yields fall, and the spread between mortgage rates and Treasurys narrows further. That is possible, but it is not guaranteed.

Even when rates improve, they may still remain historically normal by long-term standards while feeling painfully high compared with the ultra-low era of 2020 and 2021. That recent period distorted expectations. Rates below 3% were exceptional, not typical. The market today is not broken because it is not 2021. It is painful because many households built their expectations around an abnormal moment.

So yes, rates can move lower. But buyers should think in terms of “some relief” rather than “instant paradise.”

How Buyers Can Respond Without Losing Their Minds

- Shop multiple lenders: Rate quotes vary more than many buyers expect.

- Watch APR, not just the headline rate: Fees matter.

- Improve your credit profile: Better credit can mean a lower rate.

- Adjust your price range: A smaller loan can create a much safer monthly payment.

- Ask about seller concessions or builder incentives: In some markets, these can meaningfully lower upfront costs.

- Run the real monthly numbers: Taxes, insurance, HOA dues, and maintenance are not optional plot twists.

The smartest move in a high-rate environment is not chasing the perfect rate. It is building a purchase plan that still works when life does what life always does: throws in surprises.

Experience Section: What High Mortgage Rates Feel Like in Real Life

High mortgage rates are not just an economic headline. They show up in everyday decisions, private frustrations, and awkward kitchen-table math sessions that somehow always end with someone saying, “Wait, how is the monthly payment that high?”

One common experience is the first-time buyer who spent years saving for a down payment, only to realize that the monthly cost of ownership rose faster than their savings account ever could. They did everything right. They paid down debt, built credit, skipped vacations, and cut back on expenses. Then they finally got pre-approved and discovered that the house they could have comfortably afforded two or three years ago now comes with a payment that feels like it was assembled by a supervillain.

Another familiar story is the move-up buyer who owns a perfectly decent home with a wonderfully tiny mortgage rate. Their family has grown, their needs have changed, and they would like a little more space. But they run the numbers and realize that moving means trading a comfortable old payment for a dramatically larger new one. Suddenly, that extra bedroom starts competing with the idea of keeping thousands of dollars a year. The result is hesitation. Lots of hesitation. Maybe a renovation. Maybe a bunk bed. Maybe a promise to “look again next year.”

Sellers feel it too. Some list with confidence because inventory is still limited, then discover that buyers are pickier than expected. A beautiful house can still sit if the payment scares people. High rates change buyer psychology. Instead of asking, “Do I love this house?” many now ask, “Can I survive this payment and still buy groceries?” That is not exactly romantic, but it is honest.

Even people who are not moving feel the effect. Homeowners with low fixed rates often become accidental spectators, watching the market from the sidelines with a strange combination of gratitude and disbelief. They know they are lucky. They also know they are somewhat trapped. Their house may no longer fit perfectly, but their mortgage rate does. That creates a low-grade emotional tug-of-war: the freedom to move versus the fear of replacing a once-in-a-generation loan with a far more expensive one.

Then there are buyers trying to “time the market,” refreshing news alerts and mortgage charts like amateur bond traders. One day rates dip and optimism returns. The next day yields jump, a geopolitical headline lands, and the monthly payment is ugly again. It is exhausting. High mortgage rates are stressful not only because they cost more, but because they create uncertainty. People struggle more with unclear pain than known pain.

Still, there is one encouraging pattern in all these experiences. Most successful buyers stop obsessing over the perfect rate and start focusing on a sustainable payment, a realistic timeline, and a home that actually fits their life. The people who come through this market best are not the ones who predict every move correctly. They are the ones who make solid decisions with the information they have, keep enough financial breathing room, and remember that a home purchase is a long game. Mortgage rates may be high, but panic is always overpriced.

Conclusion

Mortgage rates are high because inflation concerns, elevated Treasury yields, a wider-than-normal mortgage spread, cautious Federal Reserve expectations, and limited housing supply are all working together to keep borrowing costs stubbornly elevated. That combination makes home loans expensive even when rates are lower than their recent peaks.

The good news is that this is not random. There are real, understandable forces behind high mortgage rates, and that means buyers can respond strategically instead of emotionally. Shop lenders. Know your payment ceiling. Stay realistic about the market. And remember: the goal is not to outsmart every rate move. The goal is to make a housing decision that still feels smart six months, six years, and maybe six paint colors from now.