Table of Contents >> Show >> Hide

- Net Income in One Minute

- Why Net Income Matters

- The 12 Steps to Calculate Net Income

- Step 1: Pick the Reporting Period

- Step 2: Choose an Accounting Method and Stay Consistent

- Step 3: Total Your Revenue

- Step 4: Separate Operating and Non-Operating Income

- Step 5: Calculate COGS or Direct Costs

- Step 6: Subtract Operating Expenses

- Step 7: Include Non-Cash Expenses

- Step 8: Add Non-Operating Expenses

- Step 9: Calculate Pre-Tax Income (EBT)

- Step 10: Estimate and Subtract Taxes

- Step 11: Isolate One-Time or Unusual Items

- Step 12: Finalize, Validate, and Interpret

- Worked Example A: Small E-Commerce Brand (Monthly)

- Worked Example B: Freelance Consultant (Annual)

- Worked Example C: Employee Take-Home Net Income (Monthly)

- Common Mistakes That Distort Net Income

- Implementation Checklist You Can Use This Month

- How Often Should You Calculate Net Income?

- Mini FAQ: Practical Net Income Questions

- Extended Experience Section (500+ Words)

- Conclusion

If revenue is your business’s highlight reel, net income is the full documentary cutno filters, no dramatic music, and no selective editing.

It tells you what is actually left after costs, overhead, financing, and taxes. In other words, net income answers the question that matters most:

“Are we truly profitable, or just busy?”

This guide gives you a practical, repeatable, and beginner-friendly framework in 12 steps. It works for founders, freelancers, managers,

and anyone who wants their numbers to be usefulnot decorative. You’ll also get formulas, worked examples, mistake-proofing tips,

a quick implementation checklist, and a long real-world experience section at the end.

Net Income in One Minute

Basic formula: Net Income = Total Revenue − Total Expenses

Expanded formula: Net Income = (Revenue − COGS) − Operating Expenses − Non-Operating Expenses − Taxes + Other Income

Personal version: Net Income (take-home pay) = Gross Pay − Taxes − Pre-tax Deductions − Post-tax Deductions

What Net Income Is Not

- Not cash flow: A business can show profit while cash stays tight.

- Not gross revenue: Revenue is top-line; net income is bottom-line.

- Not owner draw: Owner withdrawals don’t automatically mean the business earned enough.

Why Net Income Matters

Net income is your clearest profitability score for a specific period. It helps you track trends, test pricing, evaluate hiring plans,

prepare tax estimates, and communicate with lenders, investors, or partners. Without it, strategy becomes “vibes-based accounting.”

Entertaining? Maybe. Sustainable? Not usually.

The 12 Steps to Calculate Net Income

Step 1: Pick the Reporting Period

Choose monthly, quarterly, or annual reporting before you touch a calculator. Monthly gives operational control,

quarterly supports strategic review, and annual helps with tax and year-end analysis.

Keep period boundaries clean so comparisons remain meaningful.

Step 2: Choose an Accounting Method and Stay Consistent

- Cash basis: Income when received, expenses when paid.

- Accrual basis: Income when earned, expenses when incurred.

Neither method is magic. The win comes from consistency and clean records.

Changing methods casually makes trend analysis unreliable.

Step 3: Total Your Revenue

Collect all earned income for the period, including:

- Product sales

- Service fees

- Subscriptions

- Commissions

- Other operating revenue

If you’re self-employed, include all reportable business receipts before deductions.

Step 4: Separate Operating and Non-Operating Income

Keep core business income separate from non-core items (interest income, unusual gains, one-off sale gains).

This reveals whether your core engine is strong or if profits are being propped up by non-recurring events.

Step 5: Calculate COGS or Direct Costs

Product businesses: direct materials, production labor, and production-related costs.

Service businesses: direct delivery costs such as subcontractors and project-specific tools.

Gross Profit = Revenue − COGS (or direct costs)

Step 6: Subtract Operating Expenses

Typical operating expenses include:

- Payroll and non-direct contractor costs

- Rent and utilities

- Marketing and ad spend

- Software subscriptions

- Insurance

- Administrative and professional fees

Operating Income = Gross Profit − Operating Expenses

Step 7: Include Non-Cash Expenses

Include depreciation and amortization when applicable. They may not reduce cash immediately,

but they affect accounting profit and improve the realism of your income statement.

Step 8: Add Non-Operating Expenses

Include interest expense, financing charges, and other non-operating losses.

Many companies look healthy at operating level but weaker after financing costs are counted.

Step 9: Calculate Pre-Tax Income (EBT)

Pre-Tax Income (EBT) = Operating Income ± Non-Operating Income/Expenses

EBT is useful for performance comparison before tax effects.

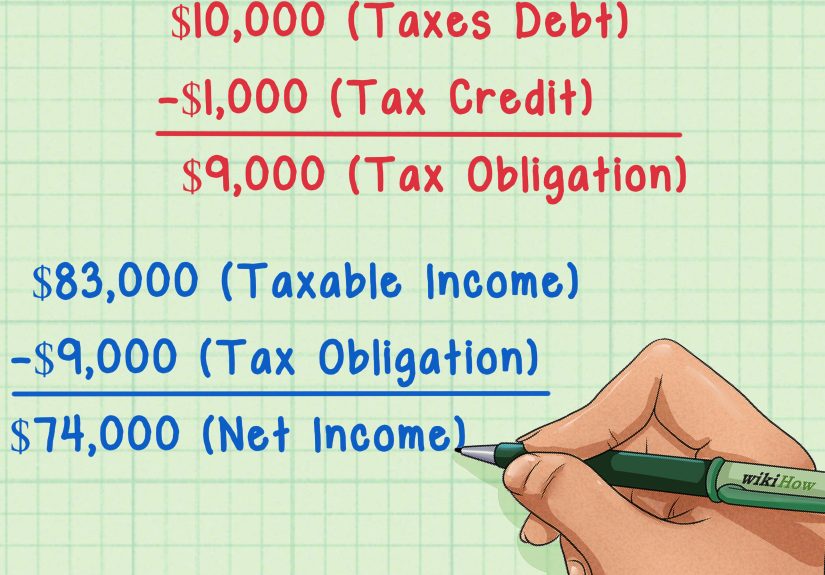

Step 10: Estimate and Subtract Taxes

Apply tax treatment based on business structure and jurisdiction. For sole proprietors and freelancers,

income tax and self-employment tax can both affect final net income.

For employees, withholding and benefit deductions shape take-home pay.

Avoid “I’ll figure taxes out later” mode. That mode reliably becomes “I am now surprised and unhappy” mode.

Step 11: Isolate One-Time or Unusual Items

Separate unusual events (settlements, disaster losses, one-time write-downs, asset sales) from normal operations.

Keep both reported and adjusted views so strategic decisions are not distorted by anomalies.

Step 12: Finalize, Validate, and Interpret

- Math check: Totals and subtotals tie correctly.

- Classification check: Expenses are in proper categories.

- Reasonableness check: Results match operational reality.

Then calculate context metric:

Net Profit Margin = Net Income ÷ Revenue × 100

Worked Example A: Small E-Commerce Brand (Monthly)

Revenue: $120,000

COGS: $48,000

Gross Profit: $72,000

Operating Expenses: $38,000

Operating Income: $34,000

Interest Expense: $2,000

Pre-Tax Income: $32,000

Estimated Taxes: $7,000

Net Income: $25,000

Net Profit Margin: 20.83%

Insight: strong margin, but it can shrink quickly if ad efficiency drops or return rates rise.

Net income should be reviewed with acquisition costs and refund trends.

Worked Example B: Freelance Consultant (Annual)

Revenue: $96,000

Direct Costs: $8,000

Gross Profit: $88,000

Operating Expenses: $12,000

Operating Income: $76,000

Interest Expense: $600

Pre-Tax Income: $75,400

Estimated Taxes: $18,850

Net Income: $56,550

Insight: revenue is healthy, but tax planning and expense tracking decide whether that top line feels strong in real life.

Worked Example C: Employee Take-Home Net Income (Monthly)

Gross Pay: $6,500

Total Deductions: $2,350 (taxes, benefits, retirement, other)

Net Take-Home Pay: $4,150

This is personal net income available for budgeting, not total compensation and not taxable income.

Common Mistakes That Distort Net Income

- Mixing personal and business expenses in one account

- Recording loan proceeds as revenue

- Ignoring accrual timing on prepaid or annual costs

- Skipping depreciation/amortization where relevant

- Underestimating taxes for variable income

- Using one unusually strong month to justify fixed-cost expansion

Implementation Checklist You Can Use This Month

If you want better numbers in the next 30 days, use this quick routine:

- Set a monthly close date and stick to it.

- Reconcile bank, card, and payment processor balances.

- Categorize every transaction before running reports.

- Separate owner draws from business expenses.

- Post recurring entries (rent, subscriptions, payroll allocations).

- Review large variances versus last month and same month last year.

- Estimate taxes and move reserves to a separate account.

- Publish a one-page profitability summary for decision makers.

This process is simple, but consistency turns it into a competitive advantage.

Clean, timely net income data enables faster pricing decisions, smarter hiring timing, and better risk management.

How Often Should You Calculate Net Income?

- Monthly: Best default for most businesses

- Quarterly: Useful for strategic planning and board updates

- Annually: Essential for tax filing and year-end benchmarking

If you only calculate net income once a year, you’re driving by rearview mirror.

Helpful for history, risky for steering.

Mini FAQ: Practical Net Income Questions

1) Is net income the same as profit?

In everyday business language, yesnet income is often called net profit or bottom-line profit.

In formal reporting, people also discuss gross profit and operating profit, so clarify which layer of profit you mean.

2) Can a company have positive net income and still struggle?

Absolutely. Profitability and liquidity are different. You can be profitable on paper but tight on cash if customers pay slowly,

inventory builds up, or debt payments hit before receivables arrive.

That is why net income should be reviewed with cash flow.

3) Should I calculate net income before or after owner compensation?

It depends on entity structure and accounting policy. The key is consistency and transparency.

If owner pay is treated differently across months, trend analysis becomes unreliable.

Keep policies documented and avoid reclassifying expenses just to make periods look better.

4) What if my net income swings wildly each month?

First, check seasonality and one-time costs. Then test pricing, variable costs, and channel mix.

Finally, review trailing 3-month and trailing 12-month views to separate noise from real structural shifts.

5) What is a good net profit margin?

There is no universal magic number. Margin targets differ by industry, model, and growth stage.

Use your own trend first, then benchmark against similar businesses.

Consistency and resilience usually matter more than one headline percentage.

Extended Experience Section (500+ Words)

In real operations, net income problems almost never come from advanced math. They come from habits: delayed bookkeeping, mixed accounts,

and “I’ll sort it out later” tax planning. Across many financial cleanups, a consistent pattern appears: people know their revenue instantly,

but hesitate when asked for net income because the number depends on categories they don’t trust yet.

That hesitation is not a character flaw. It is a systems problem.

One recurring case is the busy-but-broke business. Orders are flowing, the team is slammed, and everyone believes growth equals success.

But once expenses are categorized correctly, net income is tiny or negative. The gap usually comes from three leaks:

aggressive discounting, rising customer acquisition costs, and subscriptions purchased in moments of optimism and never removed.

Revenue looked heroic, but margins were quietly eroding. When teams switched to monthly net income reviews,

they made practical moves: repriced low-margin packages, capped ad spend on weak campaigns, and trimmed redundant software.

Profit recovered without requiring dramatic revenue growth.

Another common pattern is funding confusion. A loan closes or investment capital arrives, cash balances jump, and the organization behaves as if profitability improved.

But financing is not operating performance. If operating net income remains negative, runway still burns.

The teams that adapt fastest keep a three-line dashboard: operating net income, financing inflows, and months of runway.

This simple structure removes illusion. It also improves leadership conversations because everyone can see whether performance is improving,

not just whether cash temporarily looks comfortable.

Freelancers face a quieter version of the same challenge: tax shock. During good months, cash feels abundant, so spending grows.

Then quarterly or annual taxes arrive and confidence drops. Net income may have been positive the whole time, but cash management was not.

A practical fix is automatic tax reserving: transfer a fixed percentage from each payment into a separate tax account the same day funds arrive.

This doesn’t change accounting profit, but it changes behavior and preserves stability.

It also prevents emotional decision-making based on cash that was never truly available for discretionary spending.

Employees often discover net income complexity through pay stubs. Compensation is negotiated in gross salary,

but life is paid from take-home pay. If someone budgets using gross income, the plan fails immediately.

Reading pay stubs line by linefederal and state withholding, payroll taxes, insurance, retirement, and other deductionsturns confusion into control.

Once take-home numbers are clear, budgeting quality improves, savings rates become realistic, and debt-paydown plans finally hold.

The strongest teams and individuals share one mindset: they treat net income as feedback, not judgment.

A negative month is information. It may signal seasonality, intentional investment, temporary mix changes, or a structural pricing issue.

Instead of reacting emotionally, they diagnose line items, quantify the movement, and decide whether the cause is temporary or systemic.

Over time, this habit compounds. You reduce surprises, make better commitments, and build financial confidence.

The real payoff is not just a cleaner report; it’s better decisions under pressure.

Net income, reviewed consistently, becomes less of an accounting chore and more of a management superpower.

Conclusion

Net income is the most practical profitability metric for day-to-day leadership.

Follow the 12 steps, keep your process consistent, and pair net income with margin and cash flow analysis.

Do that, and you won’t just calculate profityou’ll build it intentionally.