Table of Contents >> Show >> Hide

- The “Attention Economy” Wants Your Money (and Your Attention)

- What the Data Says: Distraction Has a Measurable Price Tag

- The Biggest Distractions That Hijack Smart Investors

- How to Build an “Anti-Distraction” Investing System

- 1) Write a one-page Investment Policy Statement

- 2) Automate contributions and reduce decision points

- 3) Set a “portfolio checking schedule” (and stick to it)

- 4) Rebalance on a calendar, not on a feeling

- 5) Create friction for impulsive trades

- 6) Keep a small “play money” bucket (optional, but honest)

- 7) Build a smarter information diet

- 8) Use the “credential check” before trusting advice

- When You Should Pay Attention

- Conclusion: Make Investing Boring Again (Your Future Self Will Thank You)

- Experience Appendix: 5 Real-World Distraction Moments (About )

Because your portfolio doesn’t need your hot takes at 11:47 p.m.

Investing is supposed to be boring. Not “watching paint dry” boringmore like “a well-run dishwasher” boring.

You load it, you hit start, and you don’t stand there judging every swoosh of water like it’s a season finale.

Yet modern investing often feels like the opposite: alerts, breaking news banners, influencer clips, doomscrolling,

hot takes, cold takes, and that one friend who texts “ARE YOU SEEING THIS??” whenever the market sneezes.

That’s the giant distraction: turning the long, practical work of building wealth into a nonstop entertainment feed.

And the worst part? The distraction isn’t neutral. It quietly taxes returns by pushing people toward market timing,

performance chasing, overtrading, panic selling, and “I’ll just wait until things feel safe” (which is the financial

equivalent of waiting for traffic to disappear before leaving your driveway).

This article is your friendly, slightly sarcastic guide to spotting investing distractionsand building a system

that keeps you focused on what actually matters: time in the market, diversification, reasonable costs, and decisions

you can stick with through market volatility.

The “Attention Economy” Wants Your Money (and Your Attention)

The market doesn’t care if you check your portfolio 12 times a day. But lots of businesses do.

Financial media needs clicks. Social platforms need watch time. Some brokers want trades.

Some promoters want you excited (or scared) enough to buy whatever they’re selling.

The result is an ecosystem that rewards emotional investing: urgency, outrage, certainty, and FOMO.

Calm, patient investing doesn’t go viral. “Buy a diversified portfolio and rebalance once in a while” isn’t exactly a

thirst trap.

Here’s the irony: the more the world screams “PAY ATTENTION,” the more investing success depends on selective deafness.

Not ignorancedisciplined filtering.

What the Data Says: Distraction Has a Measurable Price Tag

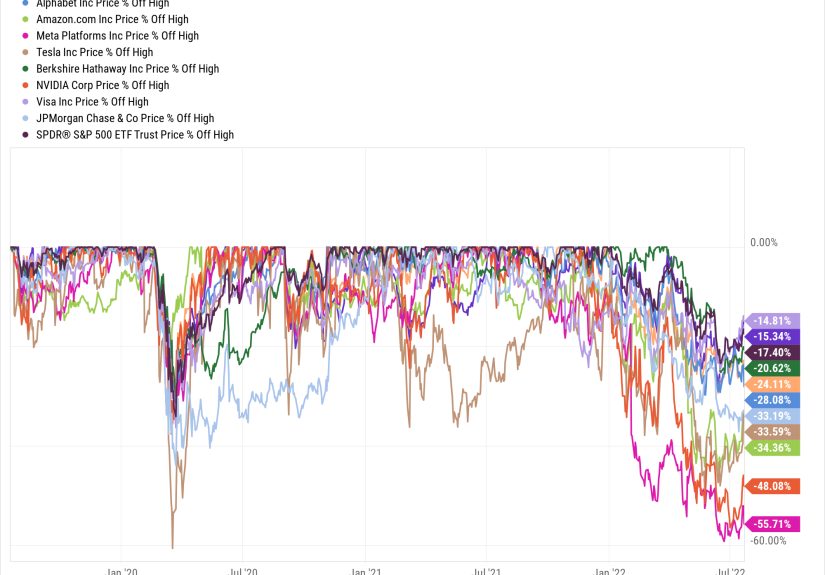

1) Market timing usually costs more than it “protects”

A classic way distractions hurt investors is by pulling them out of the market at exactly the wrong time.

One reason is that big up days often happen near big down days. When investors sell after scary drops,

they risk missing the rebound that tends to arrive when confidence is still hiding under the couch.

Research and investor education materials frequently highlight this “best days / worst days” clustering.

For example, studies shared by major firms show how missing only a small number of strong market days can

significantly reduce long-term resultsespecially over multi-decade periods.

2) The “behavior gap” is real: investors often earn less than the investments they own

The behavior gap is the difference between an investment’s reported returns and the returns investors actually earn

after their own buy/sell decisions. Think of it as the fee you pay for being human.

Morningstar’s long-running “Mind the Gap” research has documented how cash-flow timing (buying after good performance,

selling after bad performance) can reduce investor returns. In plain English: performance chasing can turn decent funds

into disappointing experiences.

3) Social-media hype can blur the line between advice, advertising, and scams

Another distraction is the rise of “finfluencers” and viral stock tips.

Some creators are well-intentioned. Some are sponsored. Some are wildly unqualified.

And some are outright scammers or impersonators.

U.S. regulators and investor-protection organizations have warned about social media stock tip scams, impersonation,

and fraudulent “investment groups” that push coordinated pump-and-dump behavior. If the pitch feels like a shortcut to

easy money, it may be a shortcut to learning a very expensive lesson.

The Biggest Distractions That Hijack Smart Investors

Headline Whiplash

Markets react to news. People overreact to market reactions. The loop is exhausting:

headline → spike or drop → “what does this mean?” → panic plan → regret.

If you can’t explain why you’re changing your strategy in one calm sentence without using the word “crash,”

you’re probably not investingyou’re reacting.

Performance Chasing (A.K.A. “Buying the Winner After the Party”)

When an asset class, sector, or single stock has already had a huge run, it becomes irresistible.

The charts look beautiful. The stories sound inevitable. Everyone suddenly has “conviction.”

Unfortunately, “everyone suddenly has conviction” is not a reliable buy signal.

Performance chasing often shows up as rotating into whatever did best recently, then rotating again,

then againlike trying to catch a bus by switching sidewalks every time you hear an engine.

Overmonitoring: Turning Investing Into a Mood Ring

Checking your portfolio constantly trains your brain to interpret normal market movement as a personal emergency.

A diversified portfolio will wiggle. That’s not a bug. That’s the market doing market things.

If daily fluctuations make you anxious, the fix is rarely “watch it more closely.” It’s usually:

better asset allocation, fewer notifications, and a plan you actually trust.

Hot Tips and “Secret” Strategies

The promise is always the same: “This one trick the pros don’t want you to know.”

Meanwhile, the most powerful toolsdiversification, low costs, tax awareness, disciplineare hiding in plain sight

like vegetables at a pizza party.

Finfluencers, Sponsored Hype, and the “Link in Bio” Trap

Some content is education. Some is marketing. Some is entertainment dressed as education.

If a creator earns money when you click, sign up, trade, or buy a course, you should assume the content is at least

partially optimized for their outcomenot yours.

Real investing is full of trade-offs: risk, time horizon, taxes, diversification, and personal goals.

Viral clips tend to flatten nuance because nuance does not get as many likes.

How to Build an “Anti-Distraction” Investing System

You don’t beat distraction with willpower. Willpower is what you use to not eat chips at 1 a.m.

You beat distraction with design: rules, defaults, and guardrails that make the right behavior easier.

1) Write a one-page Investment Policy Statement

Keep it simple. Your policy statement should answer:

- What am I investing for (goal and time horizon)?

- What is my target asset allocation (stocks/bonds/cash)?

- What would make me change it (life changes, not headlines)?

- How often will I check and rebalance?

This is not fancy paperwork. It’s your “future self” leaving instructions for your “stressed-out self.”

2) Automate contributions and reduce decision points

The more often you decide, the more often emotion gets a vote. Automating contributions (like investing each paycheck)

shrinks the space where panic can move in.

3) Set a “portfolio checking schedule” (and stick to it)

Most long-term investors do not need daily performance updates.

Consider a schedule like monthly or quarterly check-ins.

Your goal is to stay informed without becoming emotionally micromanaged by the market.

4) Rebalance on a calendar, not on a feeling

Rebalancing is one of the few “do something” actions that can be justified as disciplined investing:

trimming what grew above your target and adding to what fell below.

It’s boring. It’s mechanical. It’s the opposite of chasing shiny objects.

5) Create friction for impulsive trades

If you’re tempted to trade, introduce a waiting rule:

“I can place this trade in 48 hours if I still want it and I can explain the reason in writing.”

Many bad trades dissolve under the light of a short delay.

6) Keep a small “play money” bucket (optional, but honest)

If you love experimenting, carve out a small percentage you can afford to lose without ruining your plan.

This can reduce the urge to gamble with the retirement portion of your life.

The key is the boundary: the core portfolio stays diversified and long-term.

7) Build a smarter information diet

Try this:

- Daily: none (unless it’s your job or you’re actively learning basics).

- Weekly: one high-quality summary, not a thousand breaking-news alerts.

- Quarterly: review allocation, savings rate, and goals.

- Yearly: deeper check: taxes, fees, insurance, and major life changes.

You’re not trying to be uninformed. You’re trying to avoid being emotionally hijacked.

8) Use the “credential check” before trusting advice

Before acting on advice from a person online, ask:

- Are they licensed or registered where required?

- Do they disclose sponsorships and conflicts?

- Are they explaining risksor only promising upside?

- Would the same strategy make sense for someone with a different time horizon and goals?

If the content skips risk, it’s not education. It’s seduction.

When You Should Pay Attention

Tuning out noise doesn’t mean ignoring everything. It means focusing on the inputs that actually move long-term outcomes:

- Fees and taxes: Small percentages compound, for better or worse.

- Savings rate: Often more powerful than short-term market predictions.

- Risk level (asset allocation): The main driver of volatility you’ll experience.

- Fraud prevention: Be extra cautious with social media pitches and “exclusive groups.”

- Life changes: Job changes, family needs, major expenses, time horizon shifts.

The goal is to spend your attention on controllablesnot on guessing tomorrow’s headlines.

Conclusion: Make Investing Boring Again (Your Future Self Will Thank You)

The business of investingreal investingis about building a plan that survives reality:

recessions, bull markets, rate changes, scary headlines, viral “top picks,” and the occasional urge

to do something dramatic because your stomach did a somersault.

Distraction makes investing feel urgent. Discipline makes investing effective.

If you can automate what matters, rebalance with intention, limit the noise, and avoid the siren song of market timing,

you’ll be doing something rare: letting compounding do its job without interrupting it every time the internet gets loud.

So yesinvesting is boring. That’s the point. Your money should be working.

You should be living.

Experience Appendix: 5 Real-World Distraction Moments (About )

These are composite, true-to-life scenarios inspired by common investor experiences and advisor conversations.

1) The “I’ll Wait Until It Feels Safe” Year

An investor builds up cash because the news feels chaotic. Every week brings a fresh reason to delay: inflation one month,

layoffs the next, geopolitical stress after that. The plan becomes “wait for clarity,” but clarity never arrives on schedule.

Eventually the market rebounds while they’re still waiting for the perfect moment. When they finally invest, it’s after a long run-up,

and they feel like they “missed it.” The real issue wasn’t intelligenceit was letting emotions set the timetable.

The fix wasn’t predicting headlines; it was automating contributions and choosing an allocation they could live with.

2) The Meme-Stock Group Chat

A group chat lights up with screenshots of huge gains. The jokes are fun, the confidence is contagious,

and nobody posts their losses (mysteriously!). One investor buys in “just to be part of it,” telling themselves it’s a small bet.

Then the position grows, because they add more when the chat gets louder. When the stock drops, the chat goes quiet.

They don’t sell because it would “lock in” the mistake, so they hold and hope. Later, they realize the trade didn’t fit

any planonly the mood of the moment. If they’d kept a strict “play money” bucket, the entertainment wouldn’t have spilled

into the serious money.

3) The Finfluencer Funnel

A short video promises a “simple strategy” with eye-catching returns. The creator seems confident, the comments are hyped,

and there’s a free guidethen a paid coursethen a “VIP community.” The investor starts copying trades without understanding

the risk, because the content makes it look easy. When results disappoint, the solution offered is… buying the next product.

Eventually they step back and realize the creator’s system is designed to monetize attention, not to match the viewer’s goals.

The best move wasn’t finding a “better” influencerit was learning to verify credentials, spot conflicts, and build a plan

that doesn’t depend on someone else’s algorithm.

4) The App That Turned Investing Into a Mood Tracker

An investor checks their portfolio first thing every morning. Green days feel like a win; red days feel personal.

They start making “small adjustments” based on daily movesselling what dipped, buying what jumpedwithout realizing they’re

training themselves to trade emotionally. After a few months, they’re exhausted and their returns are worse than a simple,

diversified approach. The turning point is surprisingly basic: they turn off notifications, move to monthly check-ins,

and rebalance on a schedule. The anxiety drops. The strategy becomes sustainable. The portfolio stops being a mood ring.

5) The Calm Rebalance During the Storm

During a sharp downturn, one investor follows a written plan: they review their allocation, confirm their emergency fund,

and rebalance slightly back toward targets. No heroic predictions. No dramatic exits. No “all-in” bets. Just maintenance.

Months later, the rebound comes faster than expected, and they’re glad they stayed invested. The biggest lesson isn’t that

they “outsmarted” the marketit’s that they outsmarted their own impulse to react. That’s what anti-distraction investing looks like:

decisions made with a plan, not with adrenaline.